by

by The Government has recently tweaked the rules of Payment of Gratuity Act by bringing two amendments i.e. enhancing the limit of exemption to 20 lakhs from previous 10 lakhs and the extending the maximum maternity leave for female employees from 12 weeks to 26 weeks for determining the eligibility for qualifying as continuous service. Government is also considering reducing the Continuous Service period of eligibility from existing 5 years to 3 years. Before diving into the calculation part, let us first understand about Gratuity.

Table of Contents

What is Gratuity?

Gratuity is a Gratification or lump sum amount that your employer pays you when you retire or resign from the organization, based on the past service record of the employee. An Employee does not contribute any portion of his salary towards this amount.

It is paid out at the time of superannuation (if you retire at the age of 58) when you retire (at any other age) or resignation, and in the event of your death or being rendered disable because of an accident or illness. You need to have at least five full years of service with an employer to qualify for gratuity. This rule is relaxed in the last instance. In the event of your death, the gratuity will be paid to your nominee.

Who is Eligible?

If total period served with the current employer is less than 5 years no gratuity is payable to any individual means the employee who has completed 5 years (continuously) of his service under a current employer is eligible for Gratuity i.e. 5 years in a single organisation as prescribed under the Act.

The Payment of Gratuity Act applies to the organization employing 10 or more persons.

Calculation of Gratuity

First of all, under section 10(10) of Income Tax Act, Gratuity is tax-free for Government Employees as well as employees of local authority i.e. the whole sum received by the Government Employees and local authority employees is exempt from tax irrespective of any threshold limit.

However, in the case of non-government employees, it is taxable above a certain threshold limit.

As per the provisions of the Income Tax Act, the lowest of the below three amount shall be tax-free:

- last drawn monthly salary as on date is taken into account

- for calculation period served at a stretch with one employer is counted

- salary includes only basic pay and dearness allowance

- only commission on salary paid on the turnover basis is included

CASE-1

You are covered Under the Act:

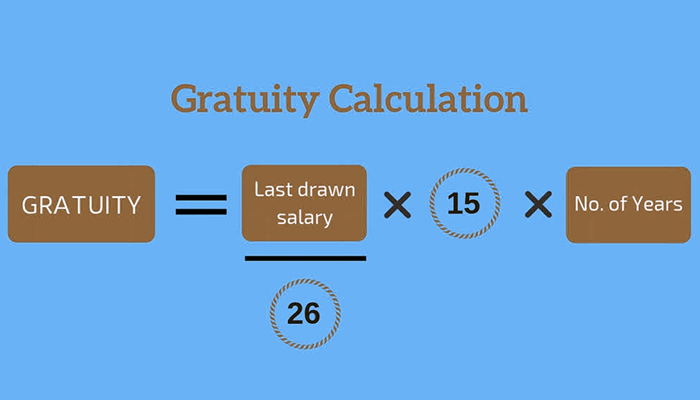

Gratuity shall be calculated as per the below formula:

Last drawn salary X 15/26 X No. of years of service

Your last drawn salary will comprise your basic + DA. Your service period will be rounded off to the nearest full year.

CASE-2

You are not covered Under the Act:

Gratuity shall be calculated as per the below formula:

Last drawn salary X 1/2 X No. of years of service

Your last drawn salary will comprise your basic + DA+ commission on sales on a turnover basis. Your service period will not be rounded off to the nearest full year. While calculating completed years, any fraction of the year will be ignored. For instance, if the employee has a total service of 20 years, 10 months and 25 days, only 20 years will be factored into the calculation.

Recommended Read: Changes in Rules of Partial Withdrawal from NPS (National Pension System)

Gratuity is computed as below:

Actual Gratuity Received Less Exemption under section 10(10)

- Actual Gratuity Received

- Last Drawn Salary X 15/26 X Completed Years of Service where salary includes basic pay + dearness allowance and for the determination of completed years of service if an employee serves more than 6 months in the last year of employment, it is considered as a full year of service.

- Maximum Amount of Rs.20 lakhs as per the amended Gratuity Act.

Among these which is least is eligible for exemption.https://www.youtube.com/embed/i31L2sCaeZY?rel=0Recommended Read: Pension, Gratuity, PF Dues Not Included in Liquidation of Assets: NCLT

Exemption under Income Tax:

- Death-cum-retirement gratuity received by employees of central or state governments and local authorities is exempt without limit.

- Gratuity received under the Payment of Gratuity Act, 1971 is exempt to the extent that it does not exceed 15 days’ salary for every completed year of service calculated on the last drawn salary subject to a maximum of Rs 20 lakhs.

- Any other gratuity is exempt to the extent that it does not exceed one half-month salary’s for each year of completed service calculated on the basis of the average salary for 10 immediately preceding months subject to a maximum of Rs 20 lakhs.

- The ceiling of Rs 20 lakhs applies to the aggregate of gratuity received from one or more employers in the same or different years.

Recommended Read: Tax on Another’s Income: Clubbing of Income

Other Points:

- Completed years of service: More than 6 months service will be counted as a full year of service i.e. 1 year 7 month will counted 2 years

- It may be noted that the number of years would be rounded off to the nearest year. Also, one needs to ensure continuous service as defined by the ACT.

- The gratuity of an employee whose services have been terminated for any act, willful omission or negligence causing any damage or loss to, or destruction of, property belonging to the employer shall be forfeited to the extent of the damage of loss so caused.

- One has to put in a minimum service of 5 years to be eligible for gratuity, however, if the employee dies then the limit may be relaxed to even one year.

- Gratuity has to be paid within 30 days from the date it becomes due. If there is a delay beyond 30 days, the employer is liable to pay simple interest at the rate notified by the Government for long term deposits.

- In case employers do not pay Gratuity, the Controlling Authority may ask the collector to collect the amount of gratuity from the employer as per section 8.

- If any employer contravenes this law, there is a penalty of Rs.10,000/- or 6 months of rigorous imprisonment or both.

Practical Approach

The Amendment in the Gratuity Act was much anticipated to bring the parity in the taxation of Gratuity between Government and Non-Government Employees. This move will surely benefit those employees who have just started their careers and stay in the organization for more than 5 years.